When software overtook metal: Are we oversleeping the automotive transition?

Automotive change: A buzzword that is being used more and more frequently these days. The automotive sector, in particular, which is so important for Germany, seems to be having difficulty getting its bearings beyond the sheet metal boundary of value creation - but things are moving. Important Personnel changes, new UNECE regulations are sending tremors through the industry, and solutions are visibly being sought in the face of material shortages and skills shortages.

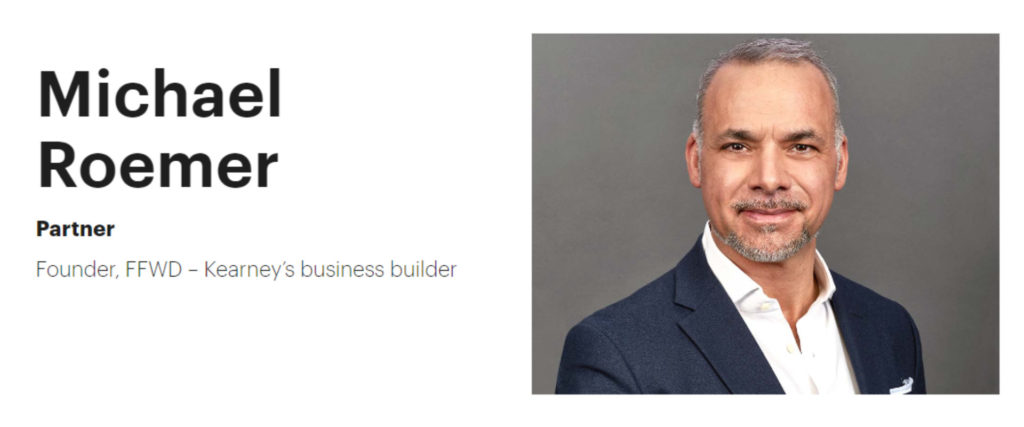

Time for us to talk to a familiar face in the industry: Michael Römer, Founder and Business Builder and well-versed in important topics such as digital transformation, growth and business building took the time to answer our pressing questions. The result is an interview that is definitely worth reading, and we hope you enjoy it and have many "aha effects".

- The interview on the automotive turnaround with Michael Römer (Kearney, Binary Core)

- "Progress in successful implementation depends on the degree of innovation."

- "The traditional OEMs are following approaches but hardly setting innovative accents."

- "CARIAD's success is immensely important to the overall success of the Group."

- "We're lagging behind and need to get back to designing new opportunities through software and electronics."

Marc

Marketing Professional

9.09.22

Ca. 16 min

The interview on the automotive turnaround with Michael Römer (Kearney, Binary Core)

Mobility Rockstars: Mr. Römer, thank you for your time. Your voice is already known in the automotive industry, has weight. What do you mean when you say that the car software industry has high disruption potential?

Michael Römer: As our daily lives become increasingly connected, customers’ expectations of the end product, the automobile, are also changing. Customers today expect a highly innovative tech product with an end-to-end and very high quality digital experience at the level of their smartphone, based on linked and fully integrated services.

The capital markets expect automakers to be able to exploit this potential for themselves – that is, to master the transformation to a technology & software group and generate additive revenues to vehicle sales through digital services and Functions on Demand. Tesla continues to be a successful example of this.

This change is redefining the value creation of automotive groups, with software replacing hardware as the primary output. The car software industry is facing unprecedented disruption, a massive shift in value creation.

This shift creates space for new market players. From Challenger OEMs, often EV players competing with traditional OEMs, to Tech players competing with traditional suppliers for software value.

That’s what I mean when I talk about disruption potential.

“Progress in successful implementation depends on the degree of innovation.”

Mobility Rockstars: What is your opinion of innovations such as UNECE R155/156 or ISO21434? How much will this change the industry, bring about an automotive change – is this even for a “software support” incl. Responsiveness prepared for decades? Has the Black Hat Hack (Grand Jeep Cherokee) shaken up the industry? Do you observe that more money is being put into research and development?

Michael Römer: The innovations set the right course for the direction of the industry. This is now followed by urgently required organizational and technical responses to legal requirements, for the secure interlocking of cyber security and the updateability of all E/E components.

However, progress in the successful implementation of these measures depends on the degree of innovation of the individual OEMs. For example, individual Challenger OEMs have been successfully implementing these measures for some time and therefore serve as guiding principles. On the other hand, there are also more traditional OEMs that are trying to move incrementally towards this model in order to address these innovations as holistically as possible.

Thus, cyber security starts with securing vehicles through “security by design”, i.e. from system architecture (robustness and updateability) to risks along the value chain to essential workflows, risk analysis and monitoring, including the supplier side. In addition, the software update management system must ensure the update capability of all electronics with all control units, meaning the safe and secure updating of vehicle software. These efforts are also being addressed with growing R&D tasks.

The explosive nature of these issues has certainly been underscored once again by the transparency of the black hat hack (Grand Jeep Cherokee).

“The traditional OEMs are following approaches but hardly setting innovative accents.”

Mobility Rockstars: Is the pace of German automotive change sufficient, or are we being left behind? Will the car lose its “Made in Germany” status and will more modern products from the Far East overtake us?

Michael Römer: According to our benchmarks, we see an increasing misalignment between Challenger and traditional OEMs, especially in the area of software value creation.

Challenger OEMs, with their clear focus on software-driven value creation, create a differentiating customer experience through an explicitly focused business model, the corresponding vehicle architecture and supplier integration. The traditional OEMs, on the other hand, merely follow these approaches, but hardly set any innovative accents.

This, along with the speed at which we push issues, needs to change. We need to create a software-based customer experience “Made In Germany” and use it to differentiate ourselves in the future. Actively exploit the design scope of disruption and meet the expectations of the capital market.

Mobility Rockstars: VW recently fired its CEO Diess, who was succeeded by Porsche CEO Blume. The reason cited is precisely that digitization is too slow. Did that surprise you despite all the pushes, or is that consistent?

Michael Römer: First of all, I wish Dr. Blume all the best for his next task and Porsche’s IPO.

Secondly, I do not want to presume to comment on the Diess personnel case in terms of the justification for this move. With his consistent orientation of VW towards the topics of electrification and software, Mr. Diess has done pioneering work for the German OEMs and thus set the right strategic course.

However, this change of course is also definitely associated with challenges in the realignment. For example, the structure of the organization in the brand network, the prioritization of topics across the individual brands and, secondly, the level of software experts/developers who really contribute to the increase in own contribution in a sufficient quality.

These issues should be part of the short-term agenda.

Mobility Rockstars: We find that interesting! So what would be your recommendation for VW’s most important steps for the “first 100 days” at the top of the decision chain?

“CARIAD’s success is immensely important to the overall success of the Group.”

Michael Römer: First of all, it’s about transparency on the short- and long-term strategic priorities. In addition, I would work to establish a strong management team that is able to make joint strategic decisions within the brand group and implement them consistently.

Among the issues, according to strategic importance and current challenges, I would prioritize these three in particular:

- Structure and process of the CARIAD organization

- Building software-driven business models and revenues

- Securing the supply chain

CARIAD’s success is immense to the overall success of the Group as a software & technology company. However, due to the central orientation, collaboration and operational development in the brand network are linked with different focuses and challenges. These must be transparently presented and adjusted. For example, a significantly higher number of native developers is needed to steer quality and in-house performance in the right direction.

In addition, the transformation to a software & technology company requires a concrete set of goals, such as “that at least thirty percent of revenues should be generated via software-driven business models by 2030.” This is the only way to ensure that the importance of this issue is sustainably anchored in the allocation of resources.

Third, I would address the issue of supply chain resilience to further ensure delivery capability – regardless of any further crises through effective risk management.

Mobility Rockstars: You said it yourself, keyword “native developers“: What the industry needs (and what is indisputably one of the biggest showstoppers of digitization in the automotive transition) are skilled workers. Nearly 100,000 positions would remain unfilled in 2021, a record aside from 2019 – a shortage of one million IT professionals is projected by 2030. IT experts, so they should help us get something like the vehicle’s operating system up and running properly or work on autonomization. Is there a real shortage of skilled workers at all, or are other industries simply more attractive in the meantime – or is there a lack of incentives from the industry, especially in the lower salary groups?

Michael Römer: The shortage of skilled workers exists, but the main factor behind the lack of skilled workers in the automotive industry is the attractiveness of the tech industry. The international struggle to attract young and very capable professionals has been in full swing for years, as you mentioned at the outset. This development is further exacerbated by the disproportionate growth of the tech industry.

The primary decision factors for young and international talent are usually: remuneration, areas of responsibility, collaboration models and environment. According to our benchmarks, the tech players score much better in all these points.

The automotive industry needs to wake up, acknowledge these points about automotive change, and finally address them. Accordingly, adapt their business model and position themselves as a tech software company. We still have very strong universities and research institutions in Germany to successfully shape this change. This means we have the best prerequisites for continuing to differentiate ourselves in international competition in the future, getting young people interested in these issues and offering them opportunities to shape their own lives.

Then I am sure that the automotive industry will become much more attractive and together we will write the next chapter of “Made in Germany”.

“We’re lagging behind and need to get back to designing new opportunities through software and electronics.”

Mobility Rockstars: Let’s stay with “Made in Germany”: Can the durability of the German automotive industry also be a quality factor that slows things down now but has an effect tomorrow? Or do we all need to become leapfrog Elon Musks to achieve automotive transformation?

Michael Römer: It takes both: consistency combined with innovation, but that doesn’t mean we all have to become Elon Musks.

For many decades, the German automotive industry has set the standard for innovation and top quality, and demonstrated consistency in this respect. I’ll give you a simple example from the recent past, Mercedes’ “SAE Level 3.” With consistency and humility, a German automotive group has launched the first certified system for highly automated driving.

But unfortunately this is an exception and cannot be applied to other software topics. In the other software domains, digital business models, etc., we unfortunately have neither innovation nor consistency nor a quality factor that will have an impact tomorrow.

We are clearly lagging behind and need to get back to actively shaping new opportunities through software and electronics and differentiating ourselves through them.

Mobility Rockstars: Thank you very much for the very interesting interview, with important insights into the status quo of the industry. Finally, our infamous “science fiction question”: If you could introduce just one change tomorrow, independently and without consultation, across the automotive industry, that would be accepted and implemented by everyone: What would it be?

Michael Römer: A joint partnership to develop a non-differentiating middleware & base OS layer. Through the synergies, we would have a very cost-effective and very high-quality approach, which would provide the industry with the necessary platform.